Structuring an employee-friendly stock option plan

⚠️ DISCLAIMER ⚠️: I am not a lawyer and this is not legal advice. Please consult an actual lawyer before adopting any of the structures discussed in this post.

Note: This post is specific to US employee stock option plans. Most of the specifics won't translate to other jurisdictions however the goals when designing a plan should.

Why care about equity incentive structures

"Show me the incentives and I will show you the outcome"

- Charlie Munger

Equity grants are the financial incentive with the largest upside team members receive when working at a startup. It ties the upside and success of the company to the teams compensation in a very direct way. If setup properly, it will greatly aide in hiring and retaining talent, and going that extra mile to ensure that it's setup in an employee-friendly way will engender loyalty from employees towards the company. They will sooner or later notice the level of care and consideration with which the plan was designed, and act accordingly.

Most founders rely on a lawyer to put together a standard employee stock option plan for them. Due to information asymmetries between legal professionals and everyone else however, the "standard" has developed to include some very employee unfriendly clauses with potentially disasterous outcomes for the very team members helping you build your company. This post will try and point out many of these sharp edges so that they can be avoided.

Goals when structuring equity incentives

- Allow early team members to have an equity setup as similar to that of founders as possible

- Reduce the chances of team members owing equity-related taxes without an offsetting sale to help pay them

- Reduce the chance an employee loses their stock options due to technicalities or gotchas

Share price dictates equity structure

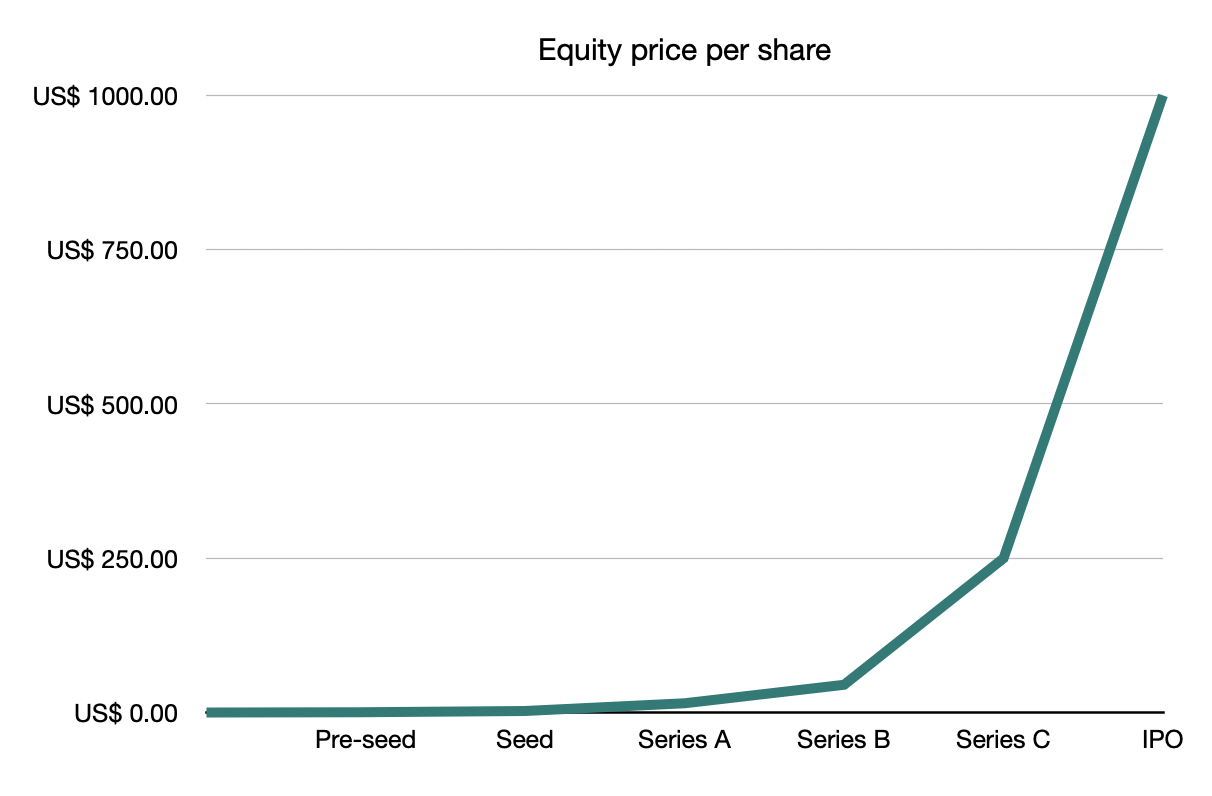

At incorporation, the shares in a newly formed entity typically start with a value of ~$0.0001 USD per share. There isn't yet a business to be valued so the shares start out being priced close to zero. As the company is built out and funds are raised, the price of the shares increases. With every successive priced round of funding, a new share price is agreed upon by the company and it's investors.

Example evolution of price per share from incorporation to unicorn status

Example evolution of price per share from incorporation to unicorn status

The share price is used for income and capital gain tax purposes. Because of this, the price of the shares at equity grant impacts the setups that make the most sense. We will now go through the various stages of the startup's lifecycle and discuss the best structures to use in each phase.

While equity is still cheap

The first shares to be issued by the company are typically those granted to the founders, and are typically issued as RSAs (restricted stock awards). RSAs are actual shares (not options) that are "restricted" in some way (usually with ~4 year vesting and a 1 year cliff). These are granted when the shares are worth fractions of a cent and can therefore be purchased outright by the founders for next to nothing. If the founders file an 83(b) election within 30 days of the grant, they pull forward any income taxes owed (which in this case would be $0 since they paid for their shares and it's value hasn't had time to go up) and will only need to contend with capital gains tax when they eventually sell their shares.

| Event | Tax Type | Tax amount |

|---|---|---|

| Grant | Income tax | $0 |

| Vest | N/A | $0 |

| Sale | Long-term capital gains | Typically ~15% |

If a founder leaves the company before fully vesting their shares, the unvested shares are returned to the company. The vested shares are already owned by the founder, and can be kept indefinitely.

For as long as possible, every startup should offer all team members the same equity structure as founders. This setup has the least number of sharp edges and the best possible tax treatment. It incentivizes early team members to act and think more like founders, adopting the company and it's mission.

Once equity becomes slightly more expensive

At some point, the FMV (fair market valuation) of the shares might rise to a point where it's cost prohibitive for employees to purchase their shares at grant (e.g., >$1000). If this happens quite early in the startup's lifecycle, you might want to consider having the company offer the employee a loan that offsets the share purchase price so that they can still benefit from the RSA structure. Both their and the company's capital outlay with the loan would be $0 and the loan can be extended to fall due after a future liquidity event. At that point in time, the employee can comfortably pay back the loan. There is an additional administrative burden for the company involved, as well as some nuanced risks with this approach, and so it will probably only make sense early on while the team is still small and the share price is still on the lower end.

Once equity becomes expensive

At some point, the equity will become too expensive for RSAs to make sense. At that point, the best alternative available is to grant ISO's (incentive stock options). Unlike RSAs, these are stock options that grant the team member the ability to purchase shares at a future date at a predetermined strike price (typically the FMV price at grant). Converting a stock option into the actual underlying stock is called exercising the option.

| Event | Tax Type | Tax amount |

|---|---|---|

| Grant | N/A | $0 |

| Vest | N/A | $0 |

| Exercise | (AMT) Alternative minimum tax | 26-28% on difference between strike price and FMV |

| Sale | Capital gains | ~15-37% |

ISO worst-case scenario

In order to better illustrate the sharp edges you'll want to remove from any incentive stock option plan at your company, let's walk through a worst-case scenarios that happen to startup employees all the time.

Lisa joined startup X early on as a founding engineer and was offered an ISO plan for 10'000 shares with a strike price of $1. After 4 years of hard work, she's decided to move back home to be closer to family and as a result leave the company. The company's ESOP (employee stock option plan) specifies that employees must exercise options within 90 days of leaving the company or otherwise forfeit them. Since the company is doing really well, the FMV for the shares has risen to $10 a share. Lisa doesn't want to miss out on the upside she's earned through her hard work so she decides to exercise. Upon exercise, Lisa would owe the IRS between $23'400 and $25'200 but her shares in the company are still illiquid so she is unable to sell them to help cover the tax bill. She'll have to pay these taxes using her savings. A year later, the startup hit a bout of bad luck and had to shutdown. Lisa was never able to sell her shares and cannot be refunded the taxes she paid at exercise.

This example points out several sharp edges common of ESOPs. The biggest is the potential for there to be a mismatch between when taxes come due and when the shares become liquid. This mismatch can force team members to forego exercising their shares and effectively lose all their hard-earned ownership in the company. The alternative option is for them to exercise and pay the resulting tax bill with savings in hopes that they will be able to sell the shares and recoup that cost at a later date. This requires them to take a big bet on the company's continued success which might not pan out.

A company can help smoothen these rough edges with multiple changes to the ESOP:

-

The startup could extend the post-termination exercise period from the standard 90 days to at least 7 years (Coinbase and Pinterest have both done exactly this). This change alone would mean Lisa wouldn't need to exercise upon leaving the company, avoiding the AMT tax consequences of doing so. There is also a greater chance the startup will have a liquidity event within those 7 years, allowing Lisa to exercise before sale, guarenteeing her liquidity with which to pay the resulting taxes.

-

The startup would offer employees the ability to early-exercise their options within 30 days of grant. If Lisa had done this, she could have filed an 83(b) election and would have had to purchase the shares from the company for $10'000 but not had to pay any income tax. This is much lower than the ~$24k that she would have owed later. In the case the startup fails, she would still lose the funds she used to purchase the shares from the company.

-

The startup could allow Lisa to sell some of her shares to investors interested in purchasing them on the secondard market. This would give Lisa the necessary liquidity to cover the outstanding tax burden and would ensure that she doesn't forfeit her hard-earned shares nor lose her savings if the startup goes under.

All three of the above can be made official in the legalese of the ESOP plan. Additionally, make sure to check that there are no draconian clawback provisions that could retroactively take back vested equity from team members. Once they've earned it, they've earned it.

Hopefully this was a helpful overview on how to best structure your company's equity to be as employee-friendly as possible. ESOP's are legal constructs and as such, can be fairly complicated. You definitely should work with a lawyer while setting one up, just make sure you don't simply copy-pasta the template they give you and call it a day. Go the extra mile to make sure your teammates are well taken care of.

If you're starting a company, and the values embodied by this post resonate with you, feel free to reach out for further advice on all things startups. I also write small angel checks.